Clarifying Accounting for Nonprofit Grants and Contracts with ASU 2018-08

In June 2018, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2018-08, Clarifying the Scope of the Accounting Guidance for Contributions Received and Contributions Made. The ASU was issued to improve the accounting guidance for nonprofits with the ultimate goal of minimizing the diversity that exists under current GAAP related to the classification of grants and contracts.

Historically, organizations have expressed difficulties in determining whether grants or similar contracts are contributions (nonreciprocal) within the scope of Topic 958, Not-for-Profit Entities, or exchange (reciprocal) transactions within the scope of other guidance, such as Topic 606, Revenue from Contracts with Customers. Many also noted challenges in determining, once a transaction is deemed to be a contribution, whether the contribution is conditional. This has resulted in variance in practice when characterizing grants and contracts of a similar nature.

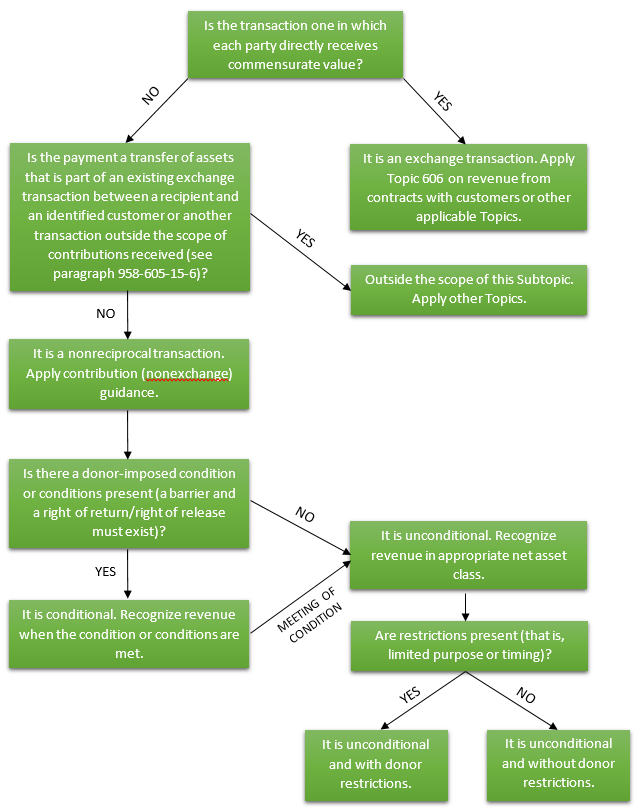

The new guidance includes the following diagram to illustrate the process for determining if a transaction is a contribution, an exchange transaction or another type of transaction, and also whether a contribution is conditional or unconditional:

Exchange or Contribution

The first step in the flowchart is determining whether the transaction is reciprocal (exchange) or nonreciprocal (contributions) based on whether or not the resource provider (i.e. grantor) receives commensurate value in return for the transferred assets. The guidance states that benefits received by the general public do not equate to commensurate value being received by the resource provider. It also clarifies that executing the resource provider’s mission does not mean commensurate value is received. These types of transactions would generally be considered nonreciprocal under the guidance of ASU 2018-08. Further, if penalties assessed on a recipient for noncompliance with terms of an agreement are limited to the delivery of assets or services already provided and/or the return of the unspent funds, the transaction would generally be indicative of a contribution (nonreciprocal).

Conditional or Unconditional Contributions

Once the organization has determined a transaction falls within the contribution guidance, the next step requires organizations to assess whether the contribution is unconditional (and recognized in revenue immediately) or conditional (with revenue recognition being deferred). In determining if a contribution is conditional, the guidance focuses on whether the following exist: (1) a barrier the recipient has to overcome to be entitled to the assets, and (2) a right of return to the contributor for assets transferred or a right of release of the promisor from its obligation to transfer assets.

The following are potential indicators and examples of barriers or conditions:

- Measurable performance-related barrier or other measurable barrier: agreement includes outcomes to be achieved within a specific time frame; recipient’s entitlement to resources is contingent upon a specified level of service, an identified number of units of output, or a specific outcome; recipient’s entitlement to resources is contingent upon an identified event (i.e. a matching requirement).

- Limited discretion by the recipient on the conduct of an activity: agreement includes requirements to follow specific guidelines about incurring expenses, requirements to hire specific individuals, or a specific protocol that must be followed.

- Stipulations related to the purpose of the agreement: agreement includes a requirement for a homeless shelter to provide a certain number of meals or an animal shelter to expand its facility to accommodate a certain number of additional animals. It is worth noting that stipulations unrelated to the purpose of the agreement are not indicative of a barrier (i.e. administrative or trivial stipulations, such as an annual reporting requirement or performance reporting requirement to demonstrate the organization took action to meet barriers listed in the agreement).

When a contribution is determined to be unconditional, the last step of the process is to determine if there are any restrictions and to recognize the revenue within the appropriate net asset class (i.e. net assets with donor restrictions or net assets without donor restrictions).

The FASB has indicated that the amendments in this ASU will likely result in more grants and contracts being accounted for as either contributions or conditional contributions than have been historically.

Effective Dates

For public business entities or not-for-profits that are conduit bond obligors, the amendments under ASU 2018-08 are effective for resource recipients for annual periods beginning after June 15, 2018. For all other entities, it is effective for annual period beginnings after December 15, 2018. Early adoption is permitted and amendments should be applied on a modified prospective basis.